New research from Metapack and Retail Economics suggests a hit to retail spending across ‘peak’ season (including Christmas, Black Friday and Cyber Monday) as cost of living crisis bites

New research from Metapack and Retail Economics suggests a hit to retail spending across ‘peak’ season (including Christmas, Black Friday and Cyber Monday) as cost of living crisis bites

UK consumers are expecting to reduce their non-essential Christmas and Black Friday spending by £4.4 billion this year as the cost-of-living crisis bites, new research from ecommerce delivery technology leader Metapack suggests. The research was commissioned by its operating company, Auctane, in partnership with retail consultancy, Retail Economics. Across the eight markets surveyed (UK, US, Germany, France, Spain, Italy, Canada and Australia), the Holiday Trends Shipping Report highlights that over $46 billion less is expected to be spent this peak season on non-food items compared to last.

The big squeeze: macroeconomic factors hit spending

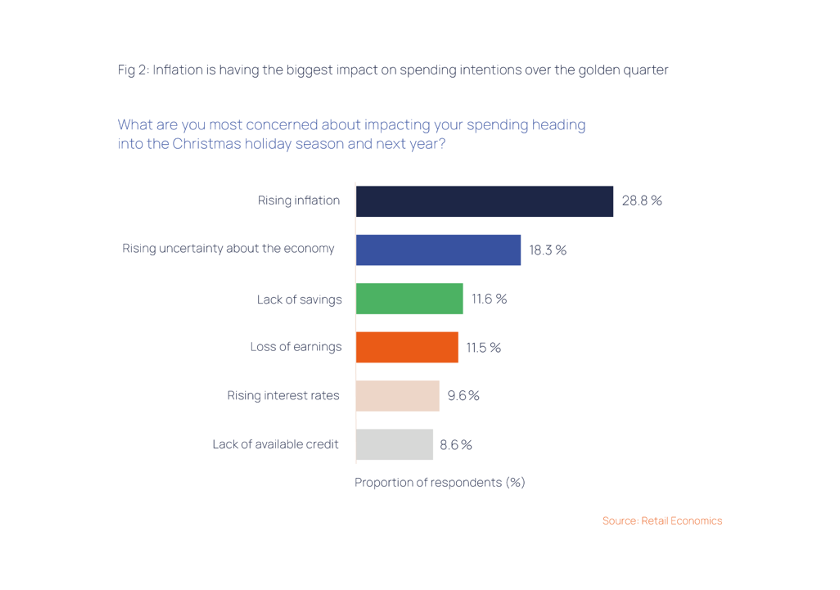

Inflation has surged to decade-highs as increasing food, fuel and energy costs squeeze consumer living standards. Almost 30% of consumers cite inflation as the biggest concern across all the markets, with 18% of consumers highlighting uncertainty about the economy and 12% concerned about a lack of savings. Alongside this, nine in 10 businesses surveyed expect to be negatively impacted by rising costs this peak season, while 58% of shoppers expect to cut back on non-food spend.

The Holiday Trends Shipping Report also identifies four key emerging shopper types as we approach the ‘golden quarter’ for the retail industry. These are categorised as: the undeterred; stretched spenders; secured but concerned; and distressed spenders. In the UK, the research highlights that 38% of consumers identify as ‘distressed’, these are shoppers who are at a high risk from rising living costs and most likely to cut back on spending. Also a further 38% of consumers identify as ‘secured but concerned’, these are shoppers who are financially strong, but their attitudes towards holiday spending are being influenced by cost of living concerns.

Retailer expectations vs consumer sentiment.

Despite the concerns around macroeconomic factors, the retailers surveyed are planning for sales volumes to increase this year. Specifically, the report highlights that 37% of large businesses are planning for an increase in volume orders compared with the previous year, with 27% of small retailers suggesting that the increase could be by more than 10%.

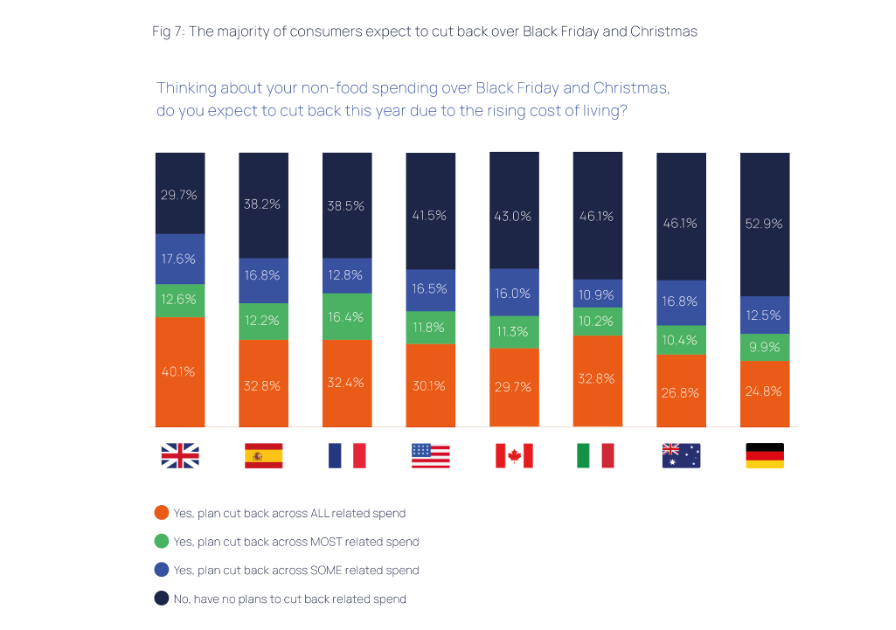

This appears to be at odds with current consumer sentiment, with 58% of shoppers expecting to cut back on spending. Consumers in the UK are expected to cut back the most, with over 70% of UK consumers expecting to reduce spending in some form.

Source: Retail Economics

Retailers are also looking at different measures to cope with rising operating costs during the busiest period of the year, with 35% stating they were looking to increase delivery costs and 26% saying they plan to make changes to delivery timeframes. Alongside this over 18% of retailers stated they would look to increase promotions and 10% are looking to eliminate free returns.

Categories facing the toughest challenge

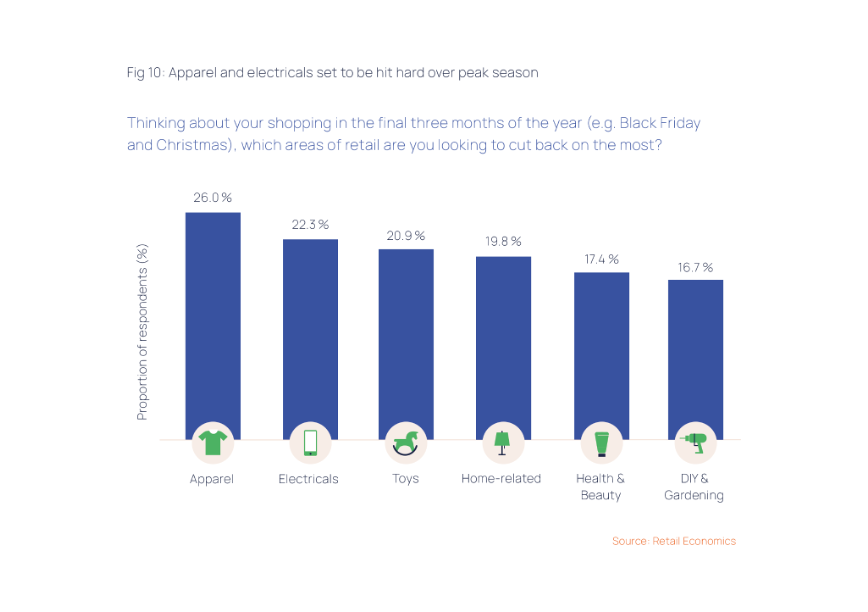

Clothing and footwear retailers look set to be hit the hardest this peak with 26% of consumers looking to cut back apparel spending. Alongside this, over 22% of consumers state that they would look to spend less on electronics. Across the markets, the least affluent are more likely than the most affluent to cut back on all Black Friday and Christmas spending this year. Across the different categories, retailers are expecting a net increase in the volume of trade this year versus last year, with furniture and flooring retailers expecting the most increase in order volumes, while electronics retailers are the most conservative overall, but are still expecting a degree of uplift on last year’s volumes.

Channel switch

Categories more at risk of cut back are also facing changes to the way consumers shop for those areas of retail. Shoppers are becoming more discerning and questioning the best channels to shop in, leading to a combination of switching between offline and online channels over the coming months as they look to get the most bang for their buck.

Specifically, household affluence is the key determinant for switching between shopping channels. The least affluent households are more likely to switch channels compared to more affluent households; while the online shift is typically being driven by more affluent consumers, especially in categories such as toys and electronics.

Richard Lim, CEO of Retail Economics: “Inflation is set to peak at exactly the wrong time for retailers. Shopper’s budgets are already under intense pressure with inflation reaching decade-highs across international markets. Consumers are concerned, budgets are under pressure, and households are intending to cut back this year as they struggle to make ends meet.

“Against this weakening consumer backdrop, retailers are also facing a pincer movement of rising input and operating costs which is testing business models to breaking point. With profit margins under intense pressure, some retailers are planning to pass on costs through delivery and returns options, precisely the areas that encourage consumers to seek out alternatives.

“Consumers will be more focused on low prices than ever during this peak period. Successful retailers will be those who double-down on their value proposition and who use data-led marketing to sensitively communicate festive joy during these difficult times.”

Andrew Norman, General Manager of Metapack: “As we head towards the festive season, consumers and retailers are facing hugely uncertain times. Rising inflation and the cost of living crisis are having a significant impact on the economy and this will dictate not only consumer spending habits but also retail strategies as they look to keep operating costs down and capitalise on what historically is the biggest shopping period of the year.

Our research highlights that retailers are forecasting growth this peak season, while consumers are looking to reduce their spending. There is a gulf that needs to be addressed between retailer expectations and consumer sentiment, and one that will need to be navigated carefully through this current economic climate. Successfully retailers should consider implementing an omni-channel strategy that appeals to a wide range of consumers. We believe proactive measures such as having a multi-carrier strategy, offering a greater choice of delivery options, such as click and collect, and offering an exceptional post-purchase delivery experience can help set retailers apart in a crowded marketplace and enable them to retain, not lose, customers this peak season.”

To find out more about what to expect this Peak season, download the full report here: Holiday Shopping Trends Report.

ENDS

Research methodology

Consumer surveys were undertaken by Retail Economics in August 2022 and include answers from a sample of more than 8,000 nationally representative consumers, additionally 800+ Auctane customers were surveyed, across the UK, USA, Canada, Australia, Germany, France, Italy and Spain.

About Retail Economics

Retail Economics is an independent economics research consultancy focused on the consumer and retail industry. We provide independent thought leadership on major economic and retail trends and analyse their impact on the industry.

Retail Economics provides proprietary data on sector growth, behavioural trends, channel performance and forecasts.